Money Dysmorphia: When Your Balance Sheet Looks Fine but Your Brain Does Not

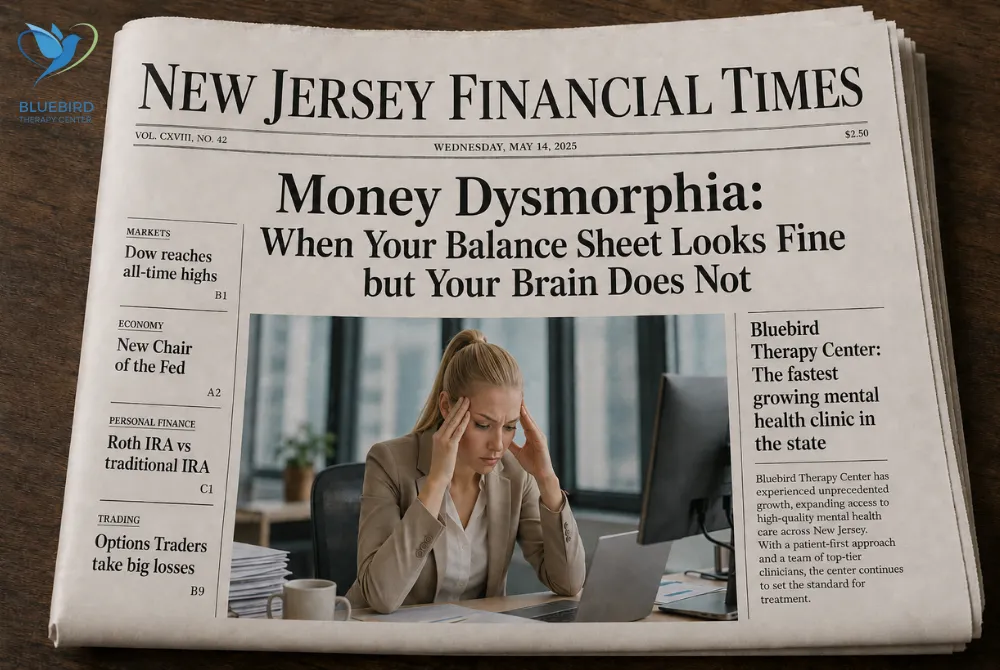

She earns six figures. Her emergency fund is capitalized. Her 401(k) contributions are on schedule and her monthly expenses clear well against her income. By every standard metric, her portfolio is performing.

And yet she checks her bank account four times a day, convinced that the numbers she is seeing cannot possibly be right. She feels, with genuine certainty, that she is one unexpected expense away from insolvency.

She is not alone. And she does not have a money problem. She has a perception problem.

The condition is called money dysmorphia, and it is quietly restructuring the mental health of many American earners.

Defining the Liability

Money dysmorphia, a term gaining significant traction in both clinical and financial advisory circles, describes a distorted perception of one's financial standing that is disconnected from actual fiscal data. Similar in structure to body dysmorphia, in which

an individual perceives physical flaws that are not objectively present, money dysmorphia produces a persistent and often paralyzing gap between financial reality and financial self-assessment.

According to a 2024 study conducted by Qualtrics on behalf of Intuit Credit Karma, 29 percent of Americans currently experience money dysmorphia, with younger demographics reporting disproportionately elevated rates. The numbers among younger market participants are particularly striking. The Credit Karma survey found that 43 percent of Gen Z and 41 percent of millennials report a distorted view of their financial health.

Perhaps the most telling data point in the entire report: 37 percent of those experiencing financial dysmorphia carry over $10,000 in savings. Their portfolios are solvent. Their perception of those portfolios is not.

This is not a balance sheet problem. This is a cognitive problem.

The Market Forces Driving the Distortion

No financial analysis is complete without examining the external pressures driving the underlying numbers, and money dysmorphia is no exception.

When the 2025 Schwab Modern Wealth Survey asked Americans how much net worth they would need to feel wealthy, millennials answered just over two million dollars while Gen Z placed that threshold at 1.7 million dollars. Yet nearly 57 percent of Gen Zers and roughly 58 percent of millennials said they were not on track to achieve those targets or did not believe they would be wealthy in their lifetimes.

The benchmark being used to assess personal financial performance is not a realistic one. It is a socially constructed projection built on curated data, specifically the highlight reel of financial aspiration served up daily by social media platforms that function, in economic terms, as a continuous comparative market feed.

Research supports this, with studies finding that people who spend over three hours per day on social media are more likely to make irrational financial decisions. The inputs are distorted. The output, an inaccurate self-assessment of financial standing, is an almost inevitable consequence.

Google searches for the term money dysmorphia increased by 136 percent between January 2024 and January 2025, suggesting that public awareness of the condition is compounding rapidly. The market for this conversation is growing.

The Real Cost to the Bottom Line

The psychological and behavioral consequences of money dysmorphia carry measurable downstream costs that extend well beyond personal discomfort.

A recent study found that 95 percent of Americans who experience money dysmorphia are negatively impacted from a financial standpoint, as the condition can lead to overspending, increased debt, and reduced savings rates. The irony is significant. The fear of financial inadequacy produces the very financial behaviors most likely to create it.

The clinical picture mirrors this. Research indicates that 86 percent of individuals with mental health conditions report that financial struggles have worsened their symptoms, while 72 percent say their mental health challenges have negatively affected their financial wellbeing, creating a self-reinforcing cycle.

This is a compounding liability. Left unaddressed, it grows. The interest rate on untreated financial anxiety is steep.

The Diagnostic Framework

Money dysmorphia presents across a recognizable set of behavioral and cognitive indicators that financial advisors and mental health professionals are increasingly trained to identify:

Compulsive account monitoring that does not produce reassurance regardless of the balances displayed

Persistent feelings of financial scarcity in the presence of objectively adequate liquidity

Avoidance of financial statements, account summaries, or any documentation that might confirm feared outcomes

Outsized emotional volatility in response to routine expenditures that fall well within established budgetary parameters

Chronic comparison of personal financial standing to externally sourced, often unverified benchmarks

Self-sabotaging fiscal behavior including unnecessary spending or excessive restriction that is rooted in emotional response rather than rational asset management

The key diagnostic marker is the disconnect. When subjective financial perception diverges materially from objective financial data, the variance is not a budgeting issue. It is a mental health issue.

The Treatment Thesis

The good news, for those inclined to think in terms of upside, is that money dysmorphia is treatable. The approach is not found in a revised budget spreadsheet or a new investment strategy. It is found in therapy.

Cognitive Behavioral Therapy is particularly well-suited to address the distorted thought patterns that drive money dysmorphia, helping individuals identify the specific cognitive errors that are producing inaccurate financial self-assessment and replace them with more accurate, calibrated thinking.

Addressing the underlying anxiety, the financial trauma history that may be informing current perception, and the comparison behaviors that are corrupting the data a person uses to evaluate their own standing are all areas where professional mental health support delivers measurable returns.

At Bluebird Therapy Center in New Jersey, we work with clients whose relationship with money is producing more anxiety than their actual financial situation warrants. We offer virtual therapy sessions for anyone across New Jersey, accept most major insurance plans, and offer a free 15-minute consultation with no commitment required.

Book your free consultation today and start recalibrating the gap between what your accounts say and what your brain believes.

The Analyst's Note

Your net worth is not your self-worth. Your account balance is not a performance review. And the financial highlight reel you are benchmarking yourself against is not an accurate market index. It is a curated fiction, and building your financial self-image against it is like valuing a company based on its best press release rather than its actual earnings.

The fundamentals of your financial life may be considerably stronger than your perception of them. Getting the right support is how you close that gap.

If you are in New Jersey and your relationship with money is costing you more than it should in anxiety, lost sleep, and daily stress, Bluebird Therapy Center is here.